FHA vs. Conventional Loans: Which Works Best for Maryland Buyers?

When you're preparing to buy your first home in the Baltimore Metro area, the how of your financing is just as important as the where of your neighborhood. The choice between an FHA loan and a Conventional loan is one of the first major decisions you'll face — and it's one that will follow you for years.

In my two decades in Maryland real estate, including years spent as an appraiser, I've seen how the wrong loan choice can cost a buyer thousands over time. My goal is to help you look past the monthly payment and see the total cost of the decision. In 2026, the gap between these two products has narrowed — but the strategy for using them remains distinct.

Quick Answer

FHA loans are typically best for Maryland buyers with credit scores between 580 and 660, or those with higher debt-to-income ratios. Conventional loans are the superior choice for buyers with scores above 720 — offering lower long-term costs and the ability to cancel mortgage insurance without refinancing.

Key Takeaways

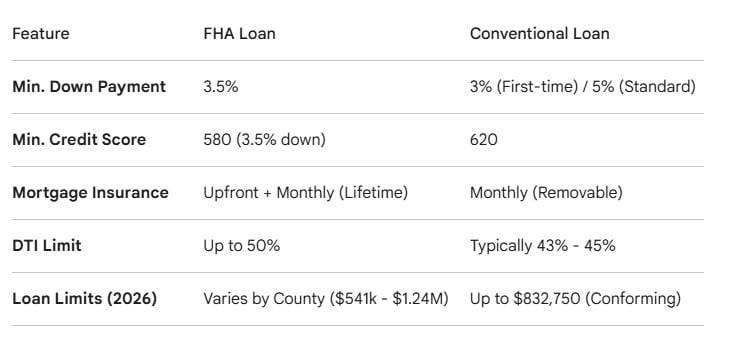

- Credit Entry: FHA allows a 3.5% down payment with a 580 score; Conventional typically requires a 620 minimum.

- Insurance Costs: FHA mortgage insurance (MIP) usually lasts the life of the loan; Conventional PMI is cancelable once you reach 20% equity.

- Property Standards: FHA appraisals are stricter on safety and health repairs — a critical factor in older Baltimore City and Baltimore County homes.

- 2026 Loan Limits: Maryland loan limits have increased for 2026, making FHA viable even in higher-priced areas like Howard County.

The Side-by-Side Comparison (2026 Maryland Data)

Understanding the technical differences takes the "sales pressure" out of the process. Here's how these two products look in today's Maryland market.

1. The Credit Score Impact

In Maryland, lenders treat credit scores as a risk-pricing tool — and the math changes significantly at certain thresholds.

- FHA Advantage: If your score is in the 600s, an FHA loan often delivers a lower interest rate than a Conventional loan would at that same score.

- Conventional Advantage: Once your score crosses 740, Conventional loans offer the best all-in pricing — including significantly cheaper private mortgage insurance (PMI).

2. The Mortgage Insurance Trap

This is where my valuation background becomes your edge. With an FHA loan, you pay an upfront premium — usually 1.75% of the loan — plus a monthly premium that typically never goes away. To stop paying it, you have to refinance.

With a Conventional loan, your PMI automatically falls off once your loan-to-value ratio reaches 78%. In a rising market like we're seeing in parts of Frederick and Carroll counties, you can often request cancellation even sooner based on a new appraisal — without refinancing at all.

3. The Appraisal Reality

FHA appraisals are essentially health-and-safety inspections in disguise. Peeling paint, missing handrails, an aging roof — these can all trigger required repairs before closing. In a competitive market, some Maryland sellers prefer Conventional offers because they perceive the appraisal process as less complicated.

As your agent, I help you navigate this by ensuring we target homes that align with your specific loan's standards — before you fall in love with a property that creates friction at the finish line.

Which Path Makes Sense for Your Situation?

You have a 640 score and 3.5% saved

Priority: Accessibility. An FHA loan is likely your best entry point. It gets you into the Maryland market now rather than waiting years to build a 740 score. We can plan a refinance exit strategy 2–3 years down the road once your equity has grown and your rate picture improves.

You have a 720+ score and 5% saved

Priority: Long-term savings. A Conventional loan is the clear winner. You'll pay less in monthly insurance, avoid the 1.75% upfront fee added to your loan balance, and have a cleaner path to removing PMI entirely.

You have significant student loan debt

Priority: DTI flexibility. FHA guidelines are often more generous toward buyers carrying high student loan balances. And programs like Maryland SmartBuy 3.0 can be paired with these loans to actually pay off qualifying student debt at closing — a powerful combination for Maryland buyers in this situation.

Frequently Asked Questions

Can I use the Maryland Mortgage Program (MMP) with both loan types?

Yes. Maryland's MMP down payment assistance can be paired with either FHA or Conventional products, provided you meet the household income requirements for your county.

What are the FHA loan limits for 2026 in Baltimore and Howard County?

For 2026, the FHA loan limit for Baltimore City, Baltimore County, Carroll County, and Howard County is $747,500. Frederick County's limit is higher at $1,249,125, reflecting its classification as a higher-cost area.

Is PMI more expensive than FHA mortgage insurance?

It depends on your credit score. For scores above 720, PMI is significantly cheaper. For scores below 660, FHA insurance is often lower in monthly cost — but it stays with you longer, which matters over a 30-year loan.

Can I buy a multi-family home with an FHA loan?

Yes — and this is one of the most underused wealth-building strategies in Maryland. You can purchase up to a 4-unit property with just 3.5% down using an FHA loan, as long as you occupy one of the units. Rental income from the other units can help offset your mortgage payment.

Do I need a 20% down payment for a Conventional loan?

No — that's one of the most persistent myths in real estate. First-time buyers can put down as little as 3% on a Conventional loan. The 20% figure simply eliminates the need for PMI entirely.

Which loan type closes faster?

There's rarely a meaningful difference in speed. Closing timelines are driven by the lender's capacity and appraisal turnaround — not by whether the loan is FHA or Conventional.

The Bottom Line: It's About Total Cost, Not Just Rate

Choosing a loan isn't just about securing the lowest rate today — it's about understanding the total cost of homeownership over the next five to ten years. My role is to help you weigh the upfront costs against the long-term flexibility so you're making a decision that serves your financial future, not just your closing date.

We don't just get you into a house. We protect the investment you're making in it.

Ready to run the numbers for your specific situation? I'd be glad to connect you with a Maryland-based lender who can produce a side-by-side Net Cost Analysis for both FHA and Conventional options — so you can see exactly what each path costs over 5, 10, and 30 years before you commit.

Get in touch and let's start the conversation.

Check out this article next