Why Multifamily Rentals Win the Math Test in Baltimore City (2026)

When I survey my investor network across Baltimore City, the debate always crystallizes around one question: does the wealth-building math favor multifamily, or is single-family simplicity the smarter edge?

Half of them insist that the classic rowhome is the backbone of the market—offering predictable exit strategies, simpler financing, and tenants who stay longer and treat the property like their own. The other half counter that single-family rentals are an amateur sandbox, arguing that small multifamily multiplexes are the only true path to scaling cash flow, consolidating capital expenditures, and insulating your portfolio against vacancy shocks.

Most real estate content answers this debate with generic platitudes: "multifamily offers scale, single-family offers simplicity."

But generic advice will cost you money in Baltimore.

Our local market operates on highly distinct economic rules. We have a city baseline property tax rate of $2.248 per $100 of assessed value—the highest in Maryland—paired with a localized legal landscape featuring ground rent structures and water utility billing nuances that can instantly break an inaccurate underwriting model. A decade of transaction analysis and 1,000+ closed files have taught me to look past investor hype and focus entirely on structural math.

To determine whether a multi-unit or single-unit footprint wins in your portfolio today, you have to unpack real-world cap rates, submarket velocity, and the operational realities of managing tenants in Baltimore City.

Quick Answer

For the current 2026 market, small multifamily properties (2 to 4 units) in Baltimore City deliver superior risk-adjusted yields, with Class B and C assets trading at cap rates between 7.5% and 9.5%. While single-family rowhomes offer lower initial operational friction and simpler conventional financing paths, multifamily assets win on pure cash flow efficiency by consolidating Baltimore's high fixed operating costs—such as property taxes and localized water utility connections—across multiple income-producing doors.

Key Takeaways

The Fixed Cost Shield: Baltimore City's $2.248 property tax rate acts as a flat penalty on low-revenue assets. Multifamily properties absorb this fixed expense more efficiently by generating multiple rent streams from a single parcel ID.

The Competitive Cap Rates: Baltimore multifamily cap rates currently average 8.5% to 9.0% for value-add portfolios, ranking among the strongest risk-adjusted yield profiles in the Mid-Atlantic region.

Vacancy Insulation Math: In a single-family rental, your vacancy rate is binary—either 0% or 100%. A duplex or triplex ensures that when a tenant transitions, the remaining units continue to service your base mortgage note and utility liabilities.

The Operational Friction: Multifamily properties introduce higher tenant turnover, shared wall disputes, and municipal licensing requirements, demanding localized property management systems to protect your net operating income (NOI).

Deconstructing the Performance Metrics

When you unpack the underwriting data from an appraisal and valuation perspective, the strategic differences between these two options reveal exactly why multifamily structures dominate for pure wealth extraction.

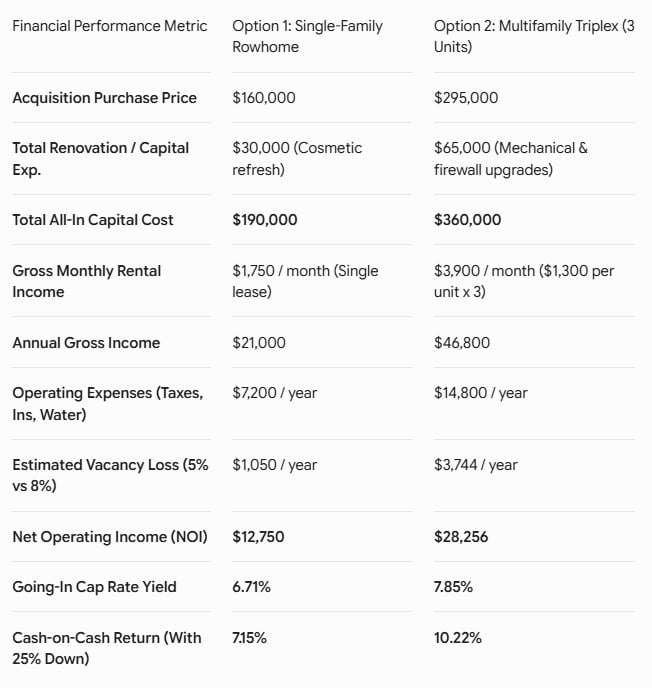

Here's the actual financial performance comparison:

The Expense Efficiency Variable

Look closely at how Baltimore's $2.248 property tax rate interacts with the two assets. In the single-family rowhome, the annual operating expenses (taxes, insurance, and water) total $7,200 on $21,000 of gross annual income—consuming 34% of your top line before vacancy and maintenance.

In the triplex, despite carrying higher total operating costs ($14,800), those expenses are spread across $46,800 of annual gross income—consuming only 32% of top line revenue. The tax burden per door drops significantly because the property occupies a single physical parcel of land, and the property tax assessment does not triple alongside the unit count. This efficiency allows a larger percentage of every dollar collected to flow directly into your net operating income ledger.

The Cap Rate Edge

Because multifamily buildings require more intense management and carry higher tenant turnover metrics, they trade at a natural risk-premium over single-family assets. This risk-premium shows up as a higher cap rate—which means higher unlevered returns.

With a going-in cap rate of 8.5% to 9.0% for Baltimore multifamily versus 6.5% to 7.0% for single-family yields, the triplex allows you to compound your capital at a faster clip. Furthermore, when you execute a value-add BRRRR renovation on a multi-unit property, every dollar you force into rent growth is multiplied across several units. This significantly impacts your final commercial valuation when you take the asset to a local bank for a cash-out refinance.

The Operational Playbook: Where First-Timers Get Tripped Up

While the math clearly favors multifamily for cash-flow generation, the physical and legal architecture of Baltimore City introduces unique operational friction points that can quickly erode your projected net operating income if left unchecked.

1. The Baltimore City Water Account Trap

In most jurisdictions, landlords can easily bill water usage back to individual tenants. In Baltimore City, the Department of Public Works (DPW) issues water bills directly to the property owner, and outstanding water balances function as a super-priority lien against the real estate title.

Most small multifamily conversions do not feature independent, city-metered water lines for each unit because digging up the street to install separate city lines can cost upwards of $10,000 per meter.

Experienced investors handle this by installing private sub-meters on the internal plumbing lines during the renovation phase. This allows you to track individual unit consumption and utilize a third-party Ratio Utility Billing System (RUBS) to legally pass the water expense back to the tenants, protecting your utility ledger from unexpected waste.

2. Fire Separation and Building Codes

Converting an old rowhome into a legal multi-unit property or updating an existing multiplex requires absolute adherence to the Baltimore City Department of Housing and Community Development (DHCD) guidelines.

You cannot simply put kitchens in bedrooms and call it a duplex. The city demands strict 1-hour fire-rated drywall barriers between units, sound-transmission class (STC) acoustic insulation, and fully independent, un-shared egress pathways to the exterior.

When your file undergoes a home inspection, your specialist must explicitly verify that the property holds an active, valid Baltimore City Multiple-Family Dwelling License. Operating a multifamily property without this formal municipal registration can result in immediate fines and strips away your legal standing to execute an eviction if a tenant stops paying rent.

Which Path Makes Sense for Your Portfolio?

Determining your investment destination requires a realistic assessment of your available capital stacks, operational infrastructure, and proximity to the asset.

Profile 1: The Out-of-State or Passive Cash-Flow Investor

Your Situation: You live outside the Central Maryland region or have a demanding career that prevents you from field-managing contractors, property managers, and regular tenant transitions.

The Priority: Maximum portfolio passivity, high asset predictability, and lower ongoing capital expenditure volatility.

The Decision: Single-Family Rentals or Turn-Key Multifamily with Professional Management. If you lack a tight, local trade network, single-family assets are far easier to monitor from a distance. The mechanical systems are standardized, tenant stays are historically longer (averaging 3 to 5 years in neighborhoods like Belair-Edison), and the exit strategy remains liquid because you can always sell the home directly to an owner-occupant buyer down the road. In these submarkets, single-family rents typically range $1,100–$1,400 per month, with days on market averaging 22–28 days for a quality property.

Profile 2: The Scalable Capital Accumulator

Your Situation: You are based locally, have access to reliable trade contractors, and want to aggressively scale your net worth by recycling your initial capital through force-multiplying renovations.

The Priority: Maximizing monthly cash-on-cash returns, optimizing tax-shield opportunities, and forcing substantial asset appreciation.

The Decision: Small Multifamily (2 to 4 Units) in Emerging Infill Corridors. Target historic conversions or small apartment assets in rapid-growth zones like Charles North, Station North, or Riverside. In Charles North, current asking prices range from $180,000 to $320,000 for a 3-unit property, with per-unit rents stabilizing near $900–$1,100 per month. Leverage localized tax incentives like the 10-year CHAP credit to freeze your property tax assessment, and concentrate your mechanical footprints (such as sharing a single roof or main sewer lateral across multiple income streams) to build a highly defensive, cash-flowing real estate business.

Frequently Asked Questions

Is multifamily better than single family in Baltimore?

For pure cash-flow efficiency and scaling velocity, multifamily wins because it spreads fixed operating costs across multiple doors. However, single-family homes offer lower turnover rates and simpler long-term liquidation paths.

What are average multifamily cap rates in Baltimore for 2026?

Multifamily cap rates in Baltimore City currently average between 5.25% for premium Class A luxury assets and up to 8.5% to 9.5% for value-add Class B/C portfolios in classic investor submarkets.

What is the current vacancy rate for Baltimore apartments?

The Baltimore-Columbia-Towson metro area currently carries a residential vacancy rate hovering near 5.8% to 6.1%, supported by constrained new construction delivery across the urban core and moderated absorption from prior years.

How does Baltimore City property tax affect multifamily underwriting?

Because the city real property tax rate is a substantial $2.248 per $100 of valuation, investors must ensure their pro formas account for this expense explicitly. Multifamily properties absorb this fixed weight better than single-family assets by generating higher gross revenues per square foot of land.

Can I buy a small multifamily property using a standard residential mortgage?

Yes. Residential financing guidelines apply to any property containing between 1 and 4 legal units. This allows you to secure highly favorable 30-year fixed conventional or low-down-payment FHA loan products, provided you intend to occupy one of the units as your primary residence. Any property with 5 or more units shifts into commercial valuation and financing parameters.

What is a legal rowhome conversion in Baltimore?

A legal conversion means the property has been formally approved by the city zoning board and DHCD to transition from a single-family occupancy use code into a multi-unit dwelling, meeting all modern fire walls, utility tracking, and safety egress regulations.

Underwrite with Absolute Certainty

The dividing line between a highly profitable urban real estate portfolio and a significant financial mistake is determined entirely before you sign a purchase agreement. If your investment strategy relies on broad real estate generalities or automated online estimates, you are leaving your capital exposed to local market friction.

Before you allocate your next investment down payment, execute this single strategic analysis:

The Fixed-Cost Underwriting Audit: Pull the exact tax history and current water billing records for your target asset directly from the municipal portals. Strip out any generic "10% for repairs, 10% for capex" filler from your spreadsheets. Map out a real-world, localized expense budget that reflects Baltimore's actual regulatory environment to see if your cash flow can truly defend itself.

If you want a data-driven advisory partner to help you evaluate local multifamily pipelines, analyze neighborhood rental comps, and build an insulated investment strategy for the Central Maryland market, let's connect.

Check out this article next