Baltimore Real Estate Investment in 2026: Where the Math Actually Works

Most Baltimore investment content tells you the city has potential.

This post tells you where the math actually works right now.

Not potential. Not trajectory. Not emerging. The specific neighborhoods where current rents, current purchase prices, and current expenses produce cash flow that justifies the investment in 2026. Real Baltimore numbers. Real rent figures. Real expense loads. Real cap rates.

One framing note before we start. Cash flow in Baltimore real estate requires honest accounting. The investors who lose money here are almost always the ones who underestimated expenses, overestimated rents, or both. Every number in this analysis uses conservative assumptions because conservative assumptions produce reliable outcomes. Optimistic assumptions produce surprises.

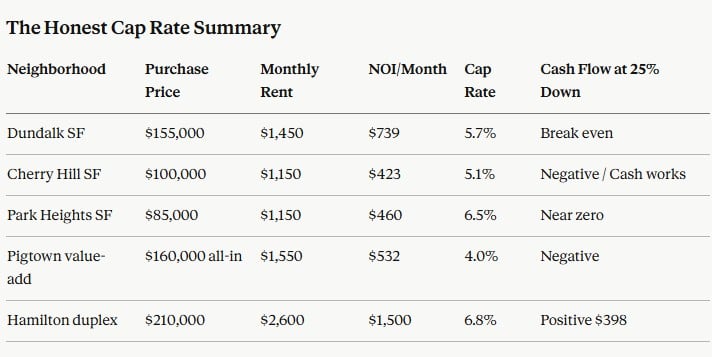

TL;DR: The Baltimore neighborhoods producing the most reliable residential rental cash flow in 2026 are Dundalk, Cherry Hill, Park Heights, Pigtown, and Hamilton-Lauraville. Each offers a distinct combination of purchase price, rent level, and expense load that produces positive cash flow for investors who buy correctly, manage proactively, and price their rents to the actual market. Single-family cash flow with conventional investor financing is extremely difficult to achieve in most Baltimore neighborhoods at current rates — small multifamily and house hacking are where the math works most consistently.

Why Baltimore Is Different From Other Cash Flow Markets

Baltimore is not a cap rate market the way Memphis or Cleveland are cap rate markets. In those markets you can buy single-family homes for $60,000 to $80,000, rent them for $900 to $1,100 per month, and achieve gross yield numbers that look extraordinary on paper.

Baltimore offers something different and in many ways more interesting — a market where purchase prices in specific neighborhoods are low enough to produce real cash flow, close enough to a major employment base to maintain consistent rental demand, and embedded in a city infrastructure of hospitals, universities, and government employment that creates durable demand that pure Rust Belt markets cannot match.

The trade-off is that Baltimore requires more active management than a passive investor wants to provide, more capital reserves than a thin-margin operator can sustain, and more neighborhood-level knowledge than an out-of-state buyer relying on a spreadsheet will ever develop. Get those three things right and Baltimore produces cash flow that most coastal markets cannot touch. Get them wrong and Baltimore produces headaches that most investors don't recover from.

The Expense Reality: What Baltimore Investing Actually Costs

This is where most Baltimore investment analyses fail. They show gross yield. They don't show what you actually keep.

Property taxes in Baltimore City run approximately $2.248 per $100 of assessed value — the highest effective rate in Maryland. On a property assessed at $100,000 that's approximately $187 per month. On a $150,000 assessed property it's $281 per month. Budget for your assessment to increase at the next triennial cycle in neighborhoods where investment activity has pushed sale prices above current assessed values.

Rental property insurance in Baltimore City runs $100 to $175 per month for a standard single-family rental depending on the property's age, condition, and location. Flood zone properties in waterfront-adjacent East Baltimore neighborhoods require separate flood insurance that can add $80 to $200 per month.

Maintenance and capital reserves are where most Baltimore investment spreadsheets get it wrong. The standard 1% annual reserve recommendation is insufficient for Baltimore City's predominantly pre-1950 housing stock. Knob and tube wiring, cast iron and galvanized plumbing, slate and flat rubber roofs, and aging mechanical systems are the baseline you're working with in most investment-grade neighborhoods. Budget 1.5% to 2% of purchase price per year. On a $120,000 purchase that's $150 to $200 per month. This reserve is not optional — it's the buffer that separates investors who survive unexpected repairs from investors who are forced to sell at the worst possible time because a furnace failed.

Property management runs 8% to 10% of gross rents for a Baltimore management company. A property generating $1,400 per month costs $112 to $140 per month in fees. If you're self-managing, assign a realistic cost to your time.

Vacancy should be budgeted at one month per year on a single-family rental and 1.5 months on a small multifamily. That's an 8% to 12.5% vacancy rate. In Baltimore's stronger rental neighborhoods with proper pricing and proactive leasing you may beat this — budget conservatively and let the actual performance be upside.

For a typical Baltimore City single-family rental generating $1,400 per month in gross rent, the full monthly expense load before debt service looks like this: property taxes $187, insurance $125, maintenance reserve $167, property management $126, vacancy allowance $117 — total $722 per month. Net operating income before debt service: $678. That is the number you finance against, not $1,400.

Neighborhood 1: Dundalk

Purchase price: $130,000–$220,000 | Average rent: $1,400–$1,650/month | Property type: Single-family detached, rowhomes

Dundalk is not Baltimore City — it's an unincorporated community in Baltimore County, and that distinction matters significantly for investors. Baltimore County's property tax rate is approximately $1.212 per $100 of assessed value compared to Baltimore City's $2.248. On the same assessed value, a Dundalk investor pays roughly half the annual property tax of a Baltimore City investor. That difference is one of the primary reasons Dundalk's cash flow numbers are stronger than comparable Baltimore City neighborhoods at similar price points.

At a $155,000 purchase price with 25% down, the loan amount of $116,250 at a 7.5% investor rate produces $813 per month in principal and interest. Against gross rent of $1,450 and a full expense load of $711, net operating income is $739 — producing a monthly cash flow of negative $74 with professional management.

Dundalk barely cash flows or breaks even at 25% down with professional management at current rates. The case here is the combination of modest positive cash flow at higher down payments, strong appreciation in a Baltimore County market posting solid year-over-year gains, tenant stability from the working-class employment base anchored by the industrial corridor and proximity to APG, and significantly lower management intensity than Baltimore City properties at comparable price points.

Investors who buy Dundalk correctly — 30% down or more, self-managed, held for five-plus years — are building meaningful equity in a market with genuine demand durability.

Cap rate: approximately 5.7% at $155,000 | Best for: Patient equity builders who want Baltimore Metro exposure without Baltimore City management complexity

Neighborhood 2: Cherry Hill

Purchase price: $80,000–$140,000 | Average rent: $1,100–$1,350/month | Property type: Single-family rowhomes, small multifamily

Cherry Hill is one of the most misunderstood investment neighborhoods in Baltimore — misunderstood in both directions. Some investors dismiss it entirely based on reputation without looking at the numbers. Others buy there without understanding the management intensity the neighborhood requires. The investors who make money in Cherry Hill go in with clear eyes about both.

The opportunity is the price-to-rent ratio. At $90,000 to $110,000 purchase prices and rents of $1,100 to $1,250 per month, Cherry Hill offers the highest gross yield numbers of any neighborhood in this analysis. The challenge is that achieving those rents with consistent occupancy requires active, attentive management and a tenant screening process more rigorous than most passive investors are prepared to implement.

At a $100,000 purchase price with 25% down, the $524 monthly payment against a net operating income of $423 produces negative $101 per month. Cherry Hill does not cash flow with conventional investor financing at current rates even at its attractive price points.

For cash buyers the picture changes: $423 per month in net operating income on a $100,000 cash purchase produces a 5.1% cash-on-cash return with meaningful upside if management is executed well and vacancy is minimized. Cherry Hill works for cash buyers or investors using creative financing structures — not for financed buyers at current rates unless purchase prices are significantly below the ranges above.

Cap rate: approximately 5.1% at $100,000 | Best for: Cash buyers or experienced Baltimore investors with existing management infrastructure

Neighborhood 3: Park Heights

Purchase price: $60,000–$130,000 | Average rent: $1,050–$1,300/month | Property type: Single-family rowhomes, some small multifamily

Park Heights generates the most investor interest in Baltimore in 2026 — and with good reason. The Baltimore Regional Neighborhood Initiative is targeting entire blocks here, not individual properties. Coordinated community investment of this kind historically precedes broader market recognition by two to three years.

The investment thesis is two-part: current cash flow at the right purchase price points and near-term appreciation driven by the concentrated public and community investment already underway. The critical variable is block-level selection. Two streets apart in this neighborhood can mean two completely different investment outcomes. Blocks receiving BRNI investment with high owner-occupancy rates offer a meaningfully different risk profile than blocks not yet targeted by revitalization capital. This is not a market where you buy from a spreadsheet.

At $85,000 on a revitalization-targeted block with 25% down, the $446 monthly payment against a net operating income of $460 produces barely positive cash flow of $14 per month. The cash flow case is secondary to the appreciation case — a Park Heights property purchased at $85,000 on an active revitalization block that reaches $130,000 in assessed value over three to five years produces an equity gain of $45,000 on a $21,250 down payment, more than a 200% return on invested equity before any cash flow is counted.

For cash buyers: $460 per month in net operating income on an $85,000 purchase produces a 6.5% cash-on-cash return — strong for a Baltimore City property in an improving corridor.

Cap rate: approximately 6.5% at $85,000 on revitalization blocks | Best for: Patient investors with block-level market knowledge comfortable with a three to five year appreciation horizon

Neighborhood 4: Pigtown (Washington Village)

Purchase price: $150,000–$260,000 | Average rent: $1,450–$1,750/month | Property type: Single-family rowhomes, some small multifamily

Pigtown has moved the furthest along the revitalization curve of any neighborhood in this analysis without yet fully pricing in that progress. It sits adjacent to the University of Maryland Medical Center complex and the Horseshoe Casino corridor, has direct access to M&T Bank Stadium and Oriole Park employment, and has been the target of sustained community investment that is visibly changing the street-level experience. The result is a neighborhood where rents have responded to the improving environment faster than purchase prices have. That gap is the investor's opportunity — and it is closing.

At $185,000 with 25% down, the $970 monthly payment against a net operating income of $582 produces negative $388 per month. Pigtown does not cash flow with conventional investor financing at current purchase prices.

The value-add scenario is more compelling. A property purchased at $130,000 needing $30,000 in renovation — all-in cost of $160,000 — renting post-renovation at $1,550 per month produces a net operating income of $532 per month and a cap rate of 4% on all-in cost. Below what other neighborhoods offer on a straight cap rate basis, but Pigtown's investment case is the intersection of a neighborhood mid-transition, growing rents, and a purchase price that hasn't yet reflected where this neighborhood is heading.

Cap rate: approximately 4%–5% depending on purchase price and renovation scope | Best for: Value-add operators with renovation capability and a three to five year hold horizon

Neighborhood 5: Hamilton-Lauraville

Purchase price: $140,000–$220,000 | Average rent: $1,400–$1,650/month | Property type: Single-family rowhomes and detached homes

Hamilton-Lauraville is Northeast Baltimore's most interesting investment market in 2026 and one of the most overlooked in the broader investor conversation. The neighborhood has genuine community infrastructure — a walkable commercial corridor on Harford Road with independent businesses, strong owner-occupancy rates that support tenant quality and property maintenance standards, and purchase prices that haven't yet moved to reflect the neighborhood's actual quality relative to comparable Baltimore City communities.

The management environment in Hamilton-Lauraville is meaningfully better than South or West Baltimore investment neighborhoods at similar price points. Tenant quality is higher, vacancy is lower, and the physical condition of the housing stock requires less intensive capital investment.

At $165,000 with 25% down, the $866 monthly payment against a net operating income of $574 produces negative $292 per month. Hamilton-Lauraville single-family doesn't produce positive monthly cash flow with conventional investor financing at current rates.

The duplex opportunity changes everything. A $210,000 duplex with 25% down produces a $1,102 monthly payment against combined gross rent of $2,600 and a combined expense load of $1,100 — net operating income of $1,500 per month, producing positive cash flow of $398 per month. This is the cash flow case in Hamilton-Lauraville. Not single-family. Duplex.

Cap rate: approximately 5.2% single-family, 6.8% duplex | Best for: Long-term equity builders who prioritize management quality, or duplex-focused investors seeking positive cash flow in a stable Northeast Baltimore corridor

Where Cash Flow Actually Lives: The Multifamily Reality

The honest truth about Baltimore residential investment in 2026 is this: single-family cash flow with conventional investor financing at 7% to 7.5% rates is extremely difficult to achieve in any Baltimore neighborhood at current purchase prices. The math works in specific scenarios — cash purchases, heavily discounted distressed acquisitions, FHA owner-occupant financing on small multifamily, seller financing at below-market rates. But the standard 25%-down-at-market-rate investor scenario does not produce positive cash flow in most Baltimore neighborhoods at 2026 price levels.

Small multifamily changes this equation significantly. A legal Baltimore City duplex at $180,000 to $220,000 with two units renting at $1,200 to $1,400 each produces gross rent of $2,400 to $2,800 per month. The expense load scales but not proportionally. A four-unit property in Baltimore City purchased at $250,000 to $320,000 with rents of $1,100 to $1,300 per unit produces gross rent of $4,400 to $5,200 per month with a cash flow profile that single-family simply cannot match.

The neighborhoods where small multifamily produces the strongest outcomes in 2026 are Hamilton-Lauraville for duplex acquisitions in a stable management environment, Waverly and Remington for three and four-unit properties in an improving corridor, and Charles Village and Barclay for student and young professional rental demand anchored by Johns Hopkins and the University of Baltimore.

The House Hack: Baltimore's Most Accessible Investment Strategy

For buyers not yet ready for a pure investment purchase, the FHA house hack remains one of the most compelling entry strategies in Baltimore's 2026 market.

FHA financing allows the purchase of up to a four-unit property with as little as 3.5% down as long as the buyer occupies one of the units as their primary residence. The rental income from the other units counts toward the buyer's qualifying income, which can significantly expand the available purchase price for a first-time investor.

In Baltimore's investment-grade neighborhoods, the house hack with FHA financing produces the strongest cash-on-cash return available to any buyer with less than $50,000 in available capital. The 3.5% down payment on a $200,000 duplex is $7,000. The rental income from the second unit immediately begins offsetting the mortgage cost. And the owner-occupant receives owner-occupied financing rates — meaningfully lower than investor rates — on a property producing rental income from day one.

The Tax Incentive Layer Most Investors Miss

Baltimore City offers a specific set of tax incentives for investment property rehabilitation that can meaningfully improve the investment math for properties in designated areas.

The Baltimore City Targeted Homeowners Tax Credit provides partial property tax abatement for renovated properties in specific incentive areas during the initial years of ownership. The High Performance Market Incentive Program provides tax credits for properties meeting specific energy efficiency standards following rehabilitation — for investors doing significant renovation work, designing the rehab to qualify can produce tax savings that improve overall returns. The Vacants to Value program provides specific incentives for investors who acquire and rehabilitate vacant city-owned properties, with below-market acquisition prices that the renovation requirement can more than justify when combined with the available tax incentives.

None of these programs are simple to navigate. But investors who understand them and factor them into their acquisition and renovation strategy consistently achieve returns that comparable investors without this knowledge cannot replicate.

Three Rules That Separate Baltimore Investors Who Build Wealth From Those Who Don't

After nearly 20 years watching investors succeed and fail in this market, three rules consistently separate the ones who build wealth here from the ones who don't.

The first is to buy the price, not the neighborhood. The most common Baltimore investment mistake is buying a property in a neighborhood you like at a price that doesn't support the investment. Affinity for a neighborhood is not an investment thesis. The numbers either work or they don't — and if they don't work at the asking price, no amount of neighborhood optimism makes them work.

The second is to budget for Baltimore, not for the national average. Baltimore's tax rate, maintenance requirements, management intensity, and vacancy risk are all higher than national averages. Investors who apply national average expense assumptions to Baltimore properties consistently discover the gap between their projections and their actual results within 18 months of acquisition.

The third is to know your block before you buy your address. Baltimore's block-level variation is more dramatic than any other market in the Baltimore Metro. The difference between two adjacent streets can mean the difference between a 95% occupancy rate and a 70% occupancy rate, between a maintenance-intensive portfolio and a stable one, between an investment that builds wealth and one that consumes it. That block-level knowledge is not available in a database.

Questions I Hear a Lot

Is Baltimore real estate a good investment in 2026? Yes for investors who approach it with realistic expense assumptions, block-level market knowledge, and a clear-eyed understanding of the management requirements. No for passive investors who expect Baltimore to perform like a low-maintenance suburban market. The returns are there for investors who understand what they're buying.

What is a good cap rate for Baltimore investment property? A cap rate of 5.5% to 7% represents a realistic range for well-located Baltimore investment properties purchased at market prices in 2026. Cap rates above 7% are available but typically require distressed acquisitions, significant renovation investment, or neighborhoods with higher management intensity and vacancy risk.

Should I buy in Baltimore City or Baltimore County for investment? Baltimore County — particularly Dundalk and Middle River — offers meaningfully lower property tax obligations that improve cash flow relative to city properties at similar price points. Baltimore City offers higher potential appreciation in revitalization corridors and a wider range of price points. The right answer depends on whether your primary goal is current cash flow or total return including appreciation.

How do I find off-market investment properties in Baltimore? The most consistently productive source is relationships with agents who specialize in the specific neighborhoods you're targeting and know which properties are coming before they're listed. The Vacants to Value program is a specific resource for below-market acquisition of city-owned vacant properties. Estate sale and probate properties represent another consistent source of below-market acquisitions in Baltimore's older neighborhoods.

What should I look for in a Baltimore property management company? Management quality varies significantly and the difference between a good company and a poor one has a direct impact on your vacancy rate, maintenance costs, and tenant quality. Ask any company you're considering for their current vacancy rate across their Baltimore City portfolio, their tenant screening criteria, and their average days-to-lease metric. Interview at least three before selecting one.

The Math Has to Come Before the Decision

Baltimore investment in 2026 is not the effortless cash flow story that some markets offer. It is a market that rewards investors who do honest math, buy at the right price, manage proactively, and understand what they're buying at the block level.

The neighborhoods in this analysis produce real returns for investors who approach them correctly. Dundalk and Hamilton-Lauraville for stable equity building with manageable management requirements. Park Heights for patient investors who understand the revitalization thesis and can read block-level signals. Cherry Hill and Pigtown for cash buyers and value-add operators with the skills to execute a more complex strategy.

In every case the return is available. In every case it requires doing the math honestly before you buy rather than hoping the math works out after. If you want to run the specific numbers for a Baltimore investment property you're considering — including block-level context that doesn't exist in any database — that's exactly the kind of conversation worth having before you make any commitments.

Check out this article next