Federal Hill vs. Belair-Edison: A Side-by-Side Underwriting Breakdown for Baltimore Investors

Browse generic real estate forums and the advice on picking an investment location is almost always the same: look for job growth, check school ratings, target low-crime corridors. Those broad metrics look fine on an introductory slide. But deploying capital based on macro-level generalizations is the fastest way to trap your cash flow in an underperforming asset.

In Baltimore City, investment returns are won or lost in the hyper-local micro-data.

Baltimore is a block-by-block market defined by sharp geographic boundaries, wide variation in tenant demographics, and a high baseline property tax rate of $2.248 per $100 of assessed value. Cross a single intersection and you can move from a premium waterfront corridor with long-tenure professional tenants directly into a high-density cash-flow sandbox with a completely different operating profile. If you apply identical underwriting parameters, rent projections, and maintenance assumptions to both sides of that line, your pro forma will fracture before your first tenant transition.

Nearly two decades in the Central Maryland market — beginning with property valuation, structural appraisal, and Broker Price Opinions — has produced one consistent framework: an urban property's real return is entirely a product of its geographic boundaries. To build a high-yield buy-and-hold operation in Baltimore, you have to abandon broad municipal generalizations and master the precise metrics that govern each submarket.

Quick Answer

Evaluating a Baltimore neighborhood for a residential rental requires a systematic analysis contrasting gross rental yield against fixed localized operational drag — the city tax rate, neighborhood vacancy velocity, and the presence of historic ground rents. In the current landscape, the strategic divide is clear. Stable high-equity urban cores like Federal Hill offer lower going-in cap rates in the 5.5%–6.5% range, with superior long-term tenant stability and liquid exit options. Working-class cash-flow corridors like Belair-Edison deliver significantly higher cap rates in the 8.5%–10.5% range at the cost of elevated management friction, higher vacancy assumptions, and a thinner secondary market if you need to exit.

Key Takeaways

- The tax weight is fixed — your revenue has to absorb it — Baltimore's property tax rate is more than double most surrounding counties. Neighborhood selection must prioritize assets that maximize rent per square foot to absorb this flat cost, or focus on properties carrying active CHAP historic tax credits.

- The institutional anchor effect is real — Rental demand shifts block by block. Underwrite your target location against its proximity to major employment anchors: Johns Hopkins Hospital, the University of Maryland Medical System, and the port and logistics corridor.

- Ground rent is not a theoretical risk — Thousands of Baltimore properties carry a leasehold structure. Before any acquisition, explicitly verify Fee Simple status through the Maryland SDAT registry and clear or redeem any outstanding ground rent during escrow.

- Lead compliance is a recurring operating cost, not a one-time box to check — Every pre-1978 rental property in Maryland requires a Full Risk Reduction certificate at each tenant change. This hits working-class neighborhoods with higher turnover disproportionately harder.

Side-by-Side Underwriting Matrix: Federal Hill vs. Belair-Edison

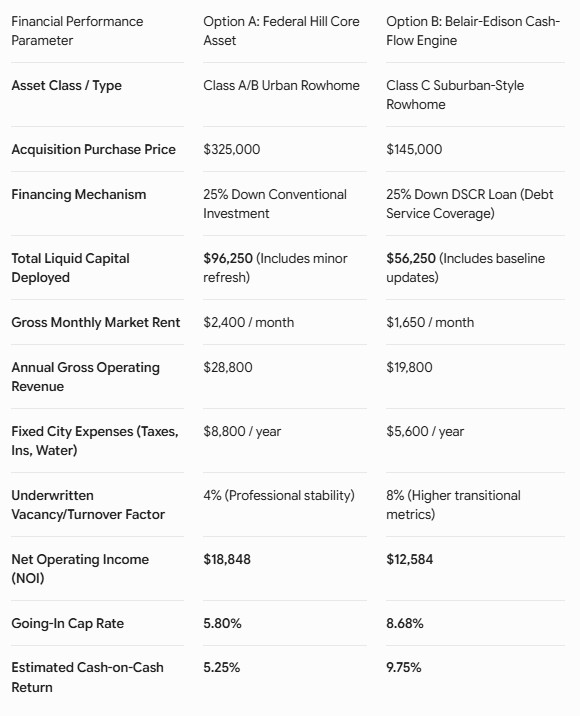

The two strategies below represent distinct buy-and-hold approaches playing out in different Baltimore zip codes. The financial parameters are drawn from the investment model accompanying this post.

Option A — The Premium High-Equity Footprint (Federal Hill, 21230)

A two-bedroom brick rowhome in a walkable waterfront district. Professional tenant profile, top-tier rents, strong equity appreciation, and a liquid exit to retail owner-occupant buyers.

Acquisition price: $325,000. Total capital deployed: $96,250 (25% down plus minor refresh). Gross monthly rent: $2,400 ($28,800 annually). Fixed city expenses (taxes, insurance, water): $8,800 per year. Underwritten vacancy factor: 4%. Net Operating Income: $18,848. Going-in cap rate: 5.80%.

Option B — The Working-Class Cash-Flow Engine (Belair-Edison, 21213)

A three-bedroom porch-front masonry rowhome in a dense residential corridor. Entry-level acquisition cost, working-class and Housing Choice Voucher tenant profile, focused on immediate dividend generation.

Acquisition price: $145,000. Total capital deployed: $56,250 (25% down DSCR loan plus baseline updates). Gross monthly rent: $1,650 ($19,800 annually). Fixed city expenses: $5,600 per year. Underwritten vacancy factor: 8%. Net Operating Income: $12,584. Going-in cap rate: 8.68%.

Note on cash-on-cash returns: The estimated cash-on-cash figures accompanying this model reflect specific financing assumptions. Investors should model their actual loan terms — rate, amortization schedule, and whether interest-only periods apply — against the NOI figures above before drawing conclusions about after-debt-service yield. At current market-rate amortizing investment loans (7%–7.5% range), Option A approaches breakeven on a cash flow basis, while Option B produces cash-on-cash returns in the 6%–7% range. Your specific terms will move these figures.

Deconstructing the Submarket Logic

The Cash-on-Cash Argument for Option B

In Belair-Edison, your capital works harder on day one in terms of gross yield and NOI per dollar deployed. The acquisition price well under $150,000 minimizes your total equity commitment, and the tenant profile — driven by local service industries, medical transport workers, and Housing Choice Voucher participants — supports rents that are high relative to that purchase price.

The trade-offs are operational: an 8% vacancy underwrite reflects real turnover dynamics in this corridor, Maryland's lead compliance cost hits every tenant transition, and property management or contractor relationships need to be local and reliable. This is not a passive asset.

The Equity Protection Argument for Option A

Federal Hill accepts a lower cap rate in exchange for transaction predictability. Professional tenants target this neighborhood for walkability to downtown employment centers, waterfront amenity, and interstate transit access. Turnover timelines are measured in years rather than months. The asset holds strong appeal for retail owner-occupant buyers — which means a clean exit at market pricing rather than an investor-to-investor discount sale.

The Federal Hill asset is not the higher-yielding play on day one. It is the higher-confidence play over a longer hold period.

Three Field Tests Before You Commit Capital

1. The Block-by-Block Occupancy and Board-Up Audit

You cannot analyze a Baltimore zip code from a spreadsheet. Drive the target street, but more importantly, drive the parallel blocks on each side and check the rear alleyways. Count occupied homes against vacant and boarded structures on the specific block. In emerging or transitional neighborhoods, more than two blighted properties on a single block escalates your vacancy risk and your maintenance exposure — vacant structures carry frozen pipe risk, pest migration, and roof interface failure that can spill into adjacent occupied assets.

2. The Maryland SDAT Ground Rent Validation Check

Go directly to the Maryland State Department of Assessments and Taxation portal and pull the raw parcel record. Confirm whether the property is held in Fee Simple or carries an active leasehold. If a ground rent is present — particularly an unregistered or unpaid one — it clouds the title chain. Your title attorney must clear or formally redeem the ground rent during escrow before you take title.

3. The Water Utility and Code Violation Diagnostic

Baltimore City water balances function as super-priority liens against the title. Outstanding balances transfer to the acquiring entity at settlement if not identified and cured. Before writing any offer, search the property through the city's E-Permits portal at dhcd.baltimorecity.gov for active housing code violations and confirm the water account status. A $3,000 water arrearage or an unresolved exterior masonry citation that surfaces post-closing belongs to you.

Which Track Fits Your Capital Position?

Your Situation: You are based outside Maryland, or your primary career limits your bandwidth for direct contractor coordination and tenant management. You want a Baltimore asset that functions as a secure, predictable long-term wealth vehicle.

Your Priority: Maximizing asset predictability and maintaining a liquid exit option.

Your Decision: Target stable, high-equity urban cores — Federal Hill, Canton, Fells Point, Locust Point. Underwrite on premium mechanical health, verified structural condition, and proximity to major medical employment anchors. Your going-in cap rate will be moderate, but you capture long hold periods, minimal property damage risk, and the ability to exit to a retail buyer rather than another investor.

Your Situation: You are locally based, hold a reliable network of licensed trade contractors, and want to maximize cash-flow velocity to scale your portfolio actively.

Your Priority: High immediate cash-on-cash yield and rapid equity scaling through forced appreciation.

Your Decision: Target working-class cash-flow corridors — Belair-Edison, Waverly, emerging pockets of Highlandtown and Pigtown. Use a DSCR loan structure to optimize leverage. Prioritize properties with updated mechanical systems: PVC plumbing, modern electrical panels, and permitted roof structures. Consider Housing Choice Voucher participation for guaranteed rent delivery on a consistent tenant base. Treat lead compliance as a line item in your operating budget, not a surprise cost.

Frequently Asked Questions

How do you evaluate a Baltimore neighborhood before buying a rental property?

The analysis requires five inputs: the block-by-block occupancy ratio, SDAT confirmation of Fee Simple vs. leasehold status, property tax impact on your NOI, the permit and code violation history on the Accela E-Permits portal at dhcd.baltimorecity.gov, and the lead compliance status of the property. Generic online data won't surface any of these.

What is a good cap rate for a Baltimore rental property?

Premium Class A/B urban core assets in established walkable neighborhoods currently trade at cap rates in the 5.5%–6.5% range. Value-add Class C residential rowhomes in working-class submarkets can produce going-in cap rates from 8.5% to 10.5% and above, depending on the specific block and acquisition price.

How does Baltimore's property tax rate affect rental underwriting?

At $2.248 per $100 of assessed value, the city tax rate is the single largest fixed overhead line in any Baltimore investment pro forma. Investors must ensure their gross rental revenue per square foot is high enough to absorb this cost without compressing net margins below their debt service threshold. Properties carrying an active CHAP credit — which offsets the tax increase on post-renovation assessed value for ten years — effectively sidestep this drag on their rehab equity for the credit term.

What is the CHAP tax credit in Baltimore investing?

The Commission for Historic and Architectural Preservation (CHAP) credit is a 10-year property tax credit that offsets the tax liability generated by the increase in assessed value following a qualifying rehabilitation. An investor who purchases at $150,000 and renovates to a $400,000 post-rehab value is taxed on the $150,000 baseline for the full 10-year credit term — a meaningful annual operating advantage over an un-credited neighboring property. The credit transfers with the property if it's sold during the term.

Can I self-manage a rental property in Baltimore City?

Yes, but regulatory compliance is non-negotiable. Every non-owner-occupied rental unit in Baltimore City must be registered and hold a valid Rental Dwelling License issued by DHCD, pass a physical inspection by a DHCD-registered inspector, and maintain an active lead certification under Maryland's Reduction of Lead Risk in Housing Act. Managing the compliance calendar — especially lead inspection timing at each tenant transition — is the primary operational demand of Baltimore self-management.

Action Plan: Underwrite the Location Before You Underwrite the Property

The return on a Baltimore investment is not determined by staging or cosmetic renovation choices. It is determined by the precision of your submarket analysis before any offer is written.

Before authorizing your agent to submit on any active Baltimore listing, run this one field check: pull up your target address and count every structure on that immediate block. Identify how many hold active residential rental licenses against those that are owner-occupied or vacant. If more than 15% of the block is blighted or unsecured, increase your vacancy and maintenance allocations upward by 4% in your model and reconfirm whether the asset can still defend its cash flow. If it can't at those revised assumptions, the deal needs more spread.

If you want a data-driven partner to help you analyze Baltimore submarket pipelines, decode land records, and build a defensible investment underwriting model for the Central Maryland market, let's connect.

Check out this article next