Bridge Loans Explained: How Maryland Buyers Keep Moving Without Stress

The most significant hurdle for Maryland homeowners looking to move up isn't finding the next house. It is the timing.

In a market like the Baltimore Metro area, where quality inventory moves fast, you often find the "perfect" home before your current one is even listed. This creates a high-stakes puzzle: How do you secure the new property without making your offer contingent on the sale of your old one?

For many, the answer is a bridge loan.

This financial tool acts as a temporary link, allowing you to access the equity in your current home to fund the down payment on the next. It removes the pressure of the "double move" and puts you in a position of strength at the negotiating table.

Quick Answer: What is a Bridge Loan in Maryland?

A bridge loan is a short-term financing option (typically 6 to 12 months) that allows homeowners to borrow against their current home's equity to purchase a new property. In Maryland, it is primarily used by move-up buyers to make non-contingent offers. Once the original home sells, the proceeds are used to pay off the bridge loan in full.

Key Takeaways

Non-Contingent Offers: Bridge loans allow you to buy before you sell, making your offer more attractive to sellers.

Short-Term Nature: These are interim loans, usually lasting less than a year.

Equity-Driven: You typically need at least 20% equity in your current home to qualify.

Cost vs. Convenience: Expect higher interest rates (often 8.5% to 11% in 2026) compared to traditional 30-year mortgages.

One Move Only: You can move directly into your new home, avoiding temporary rentals or storage units.

How Bridge Loans Work in the Maryland Market

The Maryland real estate landscape in 2026 remains competitive. With inventory levels sitting at roughly three months of supply, sellers in counties like Howard and Anne Arundel still prefer "clean" offers. A home sale contingency—where your purchase depends on you selling your house—is often a deal-breaker in a multi-offer situation.

A bridge loan solves this by providing the cash for your down payment upfront.

The Step-by-Step Process

Equity Assessment: A lender evaluates your current home's value. Most Maryland lenders require you to maintain at least 20% equity after the bridge loan is issued.

Loan Approval: The lender reviews your credit and debt-to-income (DTI) ratio. Because you may technically hold three loans at once (old mortgage, new mortgage, and bridge loan), your income must support this temporary "debt load."

The Purchase: You use the bridge loan funds for the down payment and closing costs on your new Maryland home.

The Sale: You list and sell your original home.

The Exit: You use the proceeds from the sale to pay off the bridge loan and any remaining balance on your old mortgage.

The Costs of Convenience

Bridge loans are not "cheap" money. They are specialized tools. Randy Lusk, with nearly 20 years of valuation experience through appraisals and BPOs, often reminds clients that the cost of a bridge loan should be weighed against the cost of losing your preferred home or moving twice.

Typical Fees and Rates in 2026

Interest Rates: Currently ranging from 2% to 4% above standard 30-year fixed rates.

Origination Fees: Expect to pay 1% to 2% of the loan amount.

Appraisal Fees: Since the loan is secured by your home, a professional appraisal is required.

Closing Costs: Similar to a traditional refinance, including title work and administration fees.

Perspective: If a bridge loan costs you $8,000 in interest and fees, but prevents a $12,000 double-move (temporary rental + two professional moves), the bridge loan is actually the more economical choice.

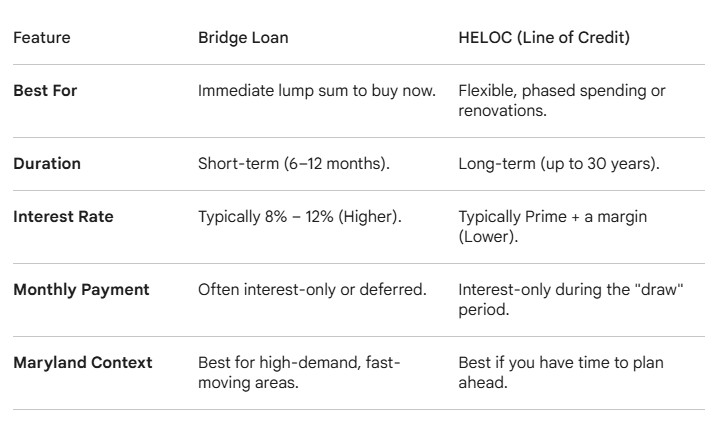

Bridge Loan vs. HELOC: Which is Better?

A common question we hear at Porchlight Property Group is whether a Home Equity Line of Credit (HELOC) is a better alternative.

The Benefit of Moving Once

Moving twice is a major stressor in real estate. You sell too fast, move into a rental, and then move again into your new house.

A bridge loan lets you move directly into your new home. Once you vacate the old property, it becomes easier to stage and show. In the Baltimore Metro market, a vacant and well-presented home often sells for a higher price than one cluttered with daily life.

Decision Framework: Problem, Priority, Decision

Use this framework to find clarity when weighing your options:

Identify the real problem : Is the issue a lack of cash for a down payment or the fear of a seller rejecting a contingent offer?

Rank what matters most : Do you prioritize the lower interest rate of a HELOC or the speed of a bridge loan?

Make the decision : If you found the right home in a fast market, the cost of a bridge loan is a small price for certainty.

Practical Advice for Maryland Homeowners

Lenders in Maryland usually require 20% equity in your current home for these programs. Most traditional lenders will not open a new HELOC once your home is listed for sale. Set this up before the sign goes in the yard.

Strategic Guidance

My role is to be the steady hand in high-stress decisions. I look at the financial architecture of your move, not just the house.

If you are planning a move in Central Maryland and feel unsure about the timing, let's talk. We can weigh the data and costs to ensure your next move is a strategic win.

Check out this article next