For many Maryland homeowners, the path to a new home starts with a high-stakes question: What should I do with the equity I’ve already built?

As you move up—whether for a better school district in Howard County or more breathing room in Frederick—you essentially have two paths. You can sell your current property to fuel your next purchase, or transform it into a rental investment. Neither is inherently "right," but in the 2026 market, one is likely more "correct" for your specific goals.

Option 1: The "Clean Break" Strategy (Selling)

Selling remains the most popular choice because it maximizes your immediate purchasing power.

The Pros:

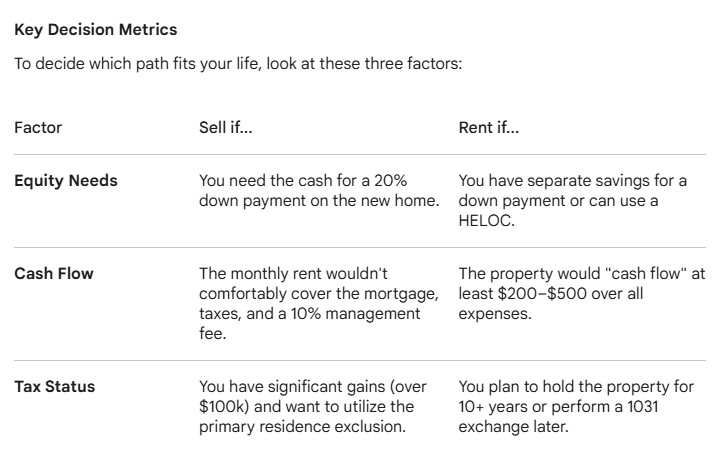

Unlocked Liquidity: With Maryland mortgage rates currently hovering around 6.1%, a larger down payment isn't just a luxury—it’s a defensive move to keep your new monthly payment manageable.

The Tax "Gift": Under current tax law, most couples can exclude up to $500,000 in capital gains ($250,000 for individuals) as long as the home was your primary residence for two of the last five years. If you rent it out for too long, you risk "aging out" of this massive tax break.

Operational Simplicity: You avoid the "3 A.M. phone call" about a leaky water heater.

The Cons:

Transaction Costs: Between commissions and closing credits, you’ll lose a percentage of your equity to the process.

Loss of Future Growth: You’re exiting a market where Maryland real estate is still seeing a steady 2-4% annual appreciation.

Option 2: The "Wealth Builder" Strategy (Renting)

With median rents in areas like Upper Marlboro hitting $2,900+ and Frederick averaging $2,300, the rental path is more lucrative than ever.

The Pros:

The Interest Rate Moat: If you’re one of the many Marylanders with a "legacy" mortgage rate below 4%, the gap between your low payment and today’s market rent is pure cash flow.

Tenant-Funded Equity: Your tenants essentially pay down your mortgage while the home’s value continues to rise.

Portfolio Diversification: You aren't just a homeowner; you’re a real estate investor with an asset that hedges against inflation.

The Cons:

Concentrated Risk: You are now responsible for two mortgages. If the rental sits vacant for two months, can your budget handle both payments?

Maintenance & Management: Being a landlord is a job. Even with a property manager (who will take ~10% of the rent), the buck ultimately stops with you.

The "Third Way": The 2026 HELOC Pivot

If you’re paralyzed by the choice, there is a middle ground. Many of my clients are using a Home Equity Line of Credit (HELOC) to "borrow" the down payment from their current home. This allows you to buy the new house first, move in, and then test the rental market. If landlording feels too heavy after six months, you can still sell.

The Bottom Line

Sell if: You want the lowest possible monthly payment on your new home and value a simplified lifestyle.

Rent if: You have a low "locked-in" interest rate and want to use your current home as a cornerstone for long-term wealth.

Not sure which path your specific property supports? The "right" move depends entirely on your home’s current value versus its projected rental yield. I can run a Real Estate Equity Report for you that compares your net proceeds from a sale against your potential monthly cash flow as a landlord.

Contact us to request your custom Equity Report and let’s look at the numbers together.

The Third Way: Tapping Equity Without Selling

If you want to keep your current home but need cash for the next one, 2026 offers several sophisticated tools. Maryland lenders are currently offering Home Equity Lines of Credit (HELOCs) that allow you to "borrow" your down payment from your current home’s equity.

This allows you to move into your new home first, then decide, without the pressure of a ticking clock, whether you’d rather find a tenant or put the old house on the market.

Final Thoughts

Choosing between selling and renting isn't just a real estate transaction; it's a portfolio decision. If you value certainty and a lower monthly payment on your next home, selling is usually the strategic move. If you value long-term asset growth and have the temperament for landlording, renting can be a cornerstone of your retirement plan.

Check out this article next