How to Pick the Right Rental Neighborhood in Harford County: A Side-by-Side Investment Analysis

If you read national real estate forums, the advice on picking an investment location is almost always the same: look for job growth, check local school ratings, find areas with low crime. Those metrics look fine on an introductory slide deck. Deploying capital based on macro-level generalizations is one of the fastest ways to trap your money in an underperforming asset.

Real estate investment returns are won or lost in the micro-data.

This is especially true in Harford County, where submarket dynamics shift completely from one zip code to the next. You can cross a single intersection or municipal boundary line and move from a premium, low-turnover family housing corridor straight into a high-density commuter rental market. If you apply the same underwriting parameters, rent projections, and vacancy assumptions to both sides of that line, your pro forma breaks before your first tenant transitions.

My approach to investment neighborhood analysis is shaped by nearly two decades in the Central Maryland sector, starting with a heavy foundational background in property valuation, structural appraisal, and Broker Price Opinions. Over 1,000 completed transactions have taught me that a property's real return is entirely a product of its geographic boundaries.

To build an insulated, high-yield buy-and-hold business, you have to abandon broad municipal assumptions and master the precise mathematical frameworks that govern regional submarkets. Here is an unvarnished, side-by-side breakdown of how to underwrite location risk and asset performance using real local data.

Quick Answer

Evaluating a neighborhood for a residential rental property requires a systematic analysis contrasting gross rental yield against fixed localized operational drag — municipal tax structure, school-tier demand, and historical tenant velocity. In the current Harford County landscape, suburban submarkets present a clear strategic divide: stable, high-equity corridors like Bel Air offer lower unlevered yields on deployed capital (roughly 5.5% to 6.5%) but superior long-term asset appreciation and minimal turnover friction, while high-velocity industrial commuter tracks like Aberdeen yield meaningfully higher unlevered returns (roughly 8.0% to 10.0%) at the cost of compressed appreciation velocity and higher physical management intensity.

Key Takeaways

- The Jurisdiction Delta Matters: Always verify municipal tax boundaries before underwriting. Buying inside an incorporated town limit introduces an additional property tax layer on top of the county base rate, which directly erodes your Net Operating Income.

- The Employment Anchor Test: Sustainable rental demand in Harford County is driven by proximity to major employment nodes — Aberdeen Proving Ground (APG), regional medical centers, and the Route 40 logistics corridor. Isolate your search around these anchors.

- School Cluster Demand Is a Retention Driver: In suburban markets, properties feeding into well-regarded school clusters attract long-term family tenants who stay through full academic cycles, reducing vacancy loss and turnover costs meaningfully compared to shorter-term commuter renters.

- Yield on Paper vs. Operations on the Ground: Higher unlevered yield on a spreadsheet frequently corresponds to higher physical maintenance intensity and faster tenant transitions. Your capital stack and management capacity must match the submarket you enter.

Side-by-Side Underwriting Matrix: Stable Suburban vs. Industrial Commuter Track

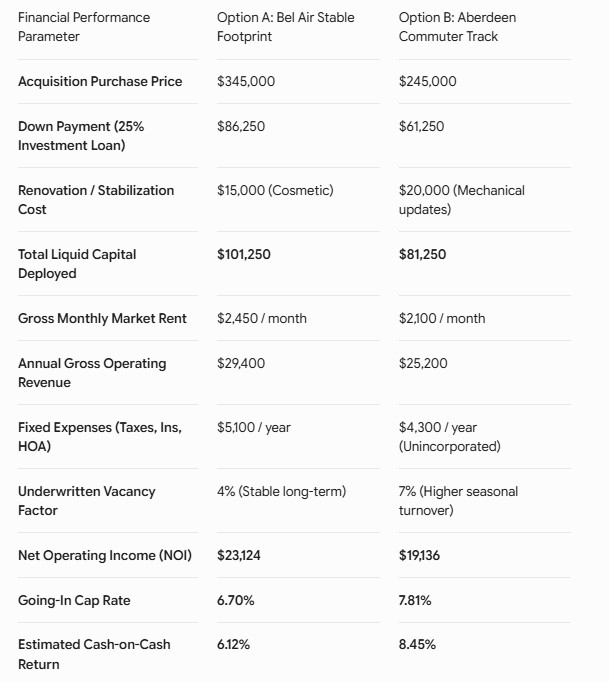

To understand how geographic variables alter your investment metrics, you need to analyze actual property footprints side by side. Below is a comparison of two standard buy-and-hold strategies playing out in distinct Harford County zip codes.

Option A — The Premium Stable Footprint (Bel Air, 21014)

This strategy targets a traditional three-bedroom townhouse or split-foyer home in an unincorporated pocket of Bel Air. It features a strong school cluster, appeals to long-term family tenants, and prioritizes equity protection and asset stability.

Option B — The Industrial Commuter Track (Aberdeen, 21001 — Unincorporated Parcels)

This strategy targets a detached rancher or townhouse configuration within the commuter pipeline of APG and the Route 40 defense and logistics corridor, specifically on parcels outside Aberdeen's incorporated city limits. It focuses on maximizing immediate income generation. Note: the 21001 zip code contains both incorporated and unincorporated parcels — investors must verify municipal boundary status for each specific address before underwriting, as incorporated parcels carry an additional municipal tax layer that would compress the NOI figures below.

Deconstructing the Submarket Data

The Income Velocity Advantage of the Commuter Track

In Option B, your capital works harder on day one. With a $100,000 lower acquisition cost, total liquid capital deployment is compressed and the unlevered yield on deployed equity runs to 8.45%.

The Aberdeen tenant demographic is driven heavily by defense contractors, military personnel transferring to APG, and regional logistics and distribution workers. This workforce demands flexible, clean, non-owner-occupied housing near major transportation corridors, which keeps gross monthly rents strong relative to purchase prices. The trade-off is a higher underwritten vacancy factor — 7% versus 4% — reflecting the shorter average tenancy cycle of commuter renters compared to family households.

The Equity Protection Logic of the Stable Corridor

In Option B, you accept a lower unlevered yield (6.12%) in exchange for transaction predictability and a lower operational management burden.

Family tenants anchored to a school system frequently stay through a full middle or high school cycle — four to six years. That directly cuts your portfolio's highest recurring expense: tenant turnover costs, which encompass paint, flooring, cleaning, and leasing commissions. Because Bel Air's unincorporated corridors carry a higher concentration of owner-occupants, the underlying asset appreciation engine remains more defensive during broader market contractions and commands a durable resale market.

The Neighborhood Evaluation Playbook: Three Field Tests

Before you submit a pre-approval letter or sign an investment property loan commitment, look past data aggregators and run these three real-world audits on any target neighborhood.

Test One: The Homeowner-to-Tenant Ratio

Drive the target street on a Tuesday afternoon and again on a Saturday morning. Observe the physical condition of the surrounding properties. Are lawns uniformly maintained? Are vehicles parked neatly in driveways, or spilling onto curbs?

A street with an owner-occupancy ratio above 70% provides a natural property management shield. Primary homeowners actively monitor the neighborhood, enforce informal behavioral standards, and protect the long-term aesthetic value of the block — all of which directly preserves your asset's exit liquidity when you eventually sell.

Test Two: The Municipal Tax Boundary Diagnostic

Go directly to the county land records or the Maryland SDAT parcel system and pull the specific parcel ID for your target address. Confirm explicitly whether the home sits within unincorporated county boundaries or inside a formal incorporated municipality.

For investors, an accidental acquisition inside town limits means a secondary municipal real estate tax stacked on top of your county tax bill, plus potential localized rental housing inspection fees. In Harford County, towns including Aberdeen, Bel Air, and Havre de Grace each levy their own municipal tax rates. A single-parcel boundary check before you underwrite eliminates this risk entirely.

Test Three: The Infrastructure and Utility Audit

Verify whether the property is connected to public water and sewer, or relies on private wells and septic systems.

For rental investors, managing a property with on-site septic and well water introduces significant capital expenditure volatility. A tenant who damages a septic drain field can trigger an immediate mandatory repair — often $10,000 to $20,000 — that wipes out multiple years of net cash flow on a single asset. Prioritize public utility connections whenever possible to keep your maintenance projections stable and predictable.

Which Investment Track Fits Your Wealth Strategy?

Your Situation: You are building long-term generational wealth through an independent entity or retirement vehicle. You want minimal daily operational involvement, low tenant turnover volatility, and an asset that functions as a durable inflation hedge.

Your Priority: Principal protection, asset predictability, and low management intensity.

Your Decision: Target stable, high-equity footprints — Bel Air, Fallston, or the Jarrettsville outskirts. Focus on core detached housing assets or premium townhomes in unincorporated corridors. Unlevered yield will be modest initially, but you capture high asset predictability, lower physical maintenance exposure, and tenant retention profiles that protect principal over a long holding horizon.

Your Situation: You live locally, hold direct relationships with reliable trade contractors, and want to compound cash income aggressively to accelerate financial independence from a traditional W-2 income stream.

Your Priority: Maximum income velocity on deployed capital with active management capacity to match.

Your Decision: Target high-velocity commuter tracks — unincorporated Aberdeen, Havre de Grace, or pockets of Abingdon and Edgewood. Look for cosmetic value-add opportunities where you can force immediate equity through mechanical updates. By keeping acquisition costs compressed and targeting the dense contractor and defense workforce pipeline along Route 40 and the APG corridor, you maximize monthly income generation and build a highly efficient cash-producing portfolio.

Frequently Asked Questions

How do you evaluate a neighborhood before buying a rental property in Harford County?

Start with submarket vacancy rates and historical rental velocity — how fast do comparable rentals lease? Then verify the owner-occupancy ratio, proximity to major employment centers, public utility infrastructure, and whether the specific parcel sits inside or outside an incorporated municipality boundary. Each of these variables affects your NOI before you write a single lease.

What is a reasonable unlevered yield target for a Harford County rental?

In the current environment, a well-underwritten suburban rental in Harford County should target an unlevered NOI yield on total equity deployed between 6.0% and 9.0%, assuming a standard 25% down investment loan structure. Actual leveraged cash flow after debt service depends heavily on your financing rate and loan terms — model both figures before committing.

How do property taxes affect rental property analysis?

Property taxes are a flat, non-negotiable fixed operating expense that reduces your Net Operating Income dollar for dollar. In Harford County, municipal boundary status matters significantly — a property inside an incorporated town pays both county and municipal real estate taxes, compressing cap rate relative to an otherwise identical parcel outside town limits.

Why do school clusters matter to real estate investors?

School cluster quality drives tenant retention. Family tenants anchored to a school system stay significantly longer than commuter renters, which lowers your portfolio's vacancy loss and turnover costs — paint, flooring, cleaning, and leasing commissions. Over a multi-year hold, the reduction in turnover expense frequently offsets the lower initial rent premium of a family-oriented corridor.

Can I use a conventional residential loan to buy a Harford County investment property?

Yes. Conventional residential lending guidelines apply to investment purchases of one to four legal units. Lenders typically require a minimum of 20% to 25% down in cash, and investment property loans carry a slightly higher interest rate premium compared to primary residence financing. Factor the actual rate environment into your debt service model before finalizing your underwriting.

Underwrite the Location Before You Underwrite the Property

The safety of a real estate investment is never determined by interior finishes. It is determined by the precision of your submarket underwriting before you step into contract. When you match your capital stack and management capacity with the correct neighborhood profile, you insulate your portfolio from the variables that sink passive investors: invisible municipal tax layers, unstable tenant demographics, and infrastructure volatility you didn't see until after closing.

Before you authorize an agent to submit an offer on an active investment listing, run this one check:

Pull the last five rental listings that closed within a half-mile radius of your target property. Ignore list prices entirely. Look only at Days on Market for those rentals. If the average time to lease exceeds 30 days, adjust your pro forma vacancy assumption from 5% to 8% and recheck whether the asset still protects your capital at that revised figure. If it does, proceed. If it doesn't, keep looking.

If you want a data-backed advisory partner to help you analyze Harford County neighborhood pipelines, verify parcel-level tax boundaries, and construct a defensible investment strategy for the Central Maryland market, reach out to Porchlight Property Group.

Check out this article next